Stone ($STNE)

(36 minutes reading)

Access to Interactive Model. Password is above disclosure.

Today’s outline

Tearsheet

Payment Segment

Upside risk for TPV Growth

Estimate market share for the big players

Funding Cost Pressure

Cash position

Virtual Debt

How much can it still hurt?

Credit Business

Loan book

Loss Ratio

Profitability

Valuation

Multiple

Free Cash Flow to Firm

Monte Carlo

Value Attribution

Net income sensibility to rates

What drives value in the long-term

Tearsheet

The first post on Stone (“STNE,” “$STNE”) was written in November and was calling for a potential downside scenario, even though stocks had fallen from $90 to $20.

Months later, the stock almost hit $10/shs, so it’s time for a new review. Indeed, I was right in my first call, but it’s rare to find a company with such qualitative characteristics as Stone has.

As I promised before, posts will be shorter than they used to. For that, I’ll comprise a lot of information, assuming that my readers have already read the first post on Stone.

All in, STNE 0.00%↑ will likely continue to face challenges in posting significant earnings expansion. First, the company suspended the origination in its credit business after issues with the receivables chambers, postponing monetization.

Second, Brazilian Central Bank has been increasing interest rates (+875bps in the cycle so far), pressuring Stone’s financial expenses and pass-through in prices.

Third, Stone has been signalizing to the market higher selling expenses from now on. In my view, low-hanging fruits are over, so incremental merchants’ addition should come at higher costs.

Nevertheless, the market might have punished the stock more than it should have, as operations are coming back to the track, and long-term drivers are mostly intact.

Payment Segment

Gathering the information provided by the large acquirer’s companies and the data provided by ABECS, the main highlights for 2021:

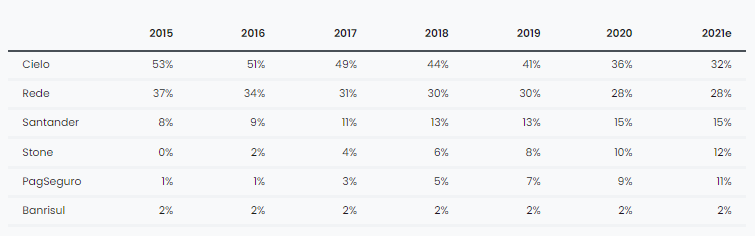

New entrants are still gaining market share from incumbents (+200bps in the year). It’s interesting to notice, but Getnet lost market share throughout the year, even though the feedback I heard was that the company was going strongly in commercial propositions.

STNE and PAGS were the main highlights. STNE lost share in the first half of the year, but PAGS has shown significant share gain along the year.

ABECS is pointing to a 30% growth in the industry TPV for 2021, versus the 24%expected by the beginning of the year. For 2022, ABECS expects another strong year, with a 24% growth (vs. 2021).

In the first half of the year, Stone lagged in growth due to capital reallocation decisions. However, it has been gaining share in the second half of the year.

Keep in mind the Stone’s market share evolution over the past five years. I think the company will sustain the pace (+200bps) for the foreseeable future.

However, the company has been pointing out that the cost of acquiring customers has also been increasing.

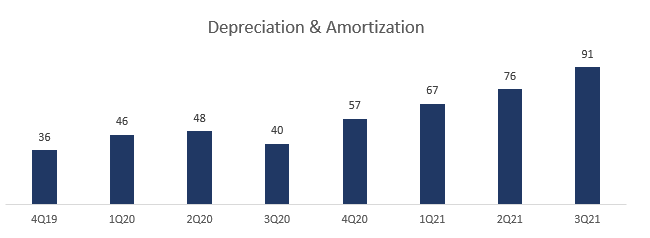

Stone’s CAC (Customer Acquisition Cost) invests in hubs and POS hardware. Therefore, the increase, or decrease, in the D&A could foresee how aggressive the company is about future investments.

Since you’ve received my stuff since last year, why don’t you redeem a free trial coupon?

One might discuss that Stone is looking for a share greater than 200bps in 2022, and the actual CAC is the same, but I don’t see it this way. As we’ll discuss later on, Stone’s cash availability will be limiting its growth over the following years.

Funding cost pressure

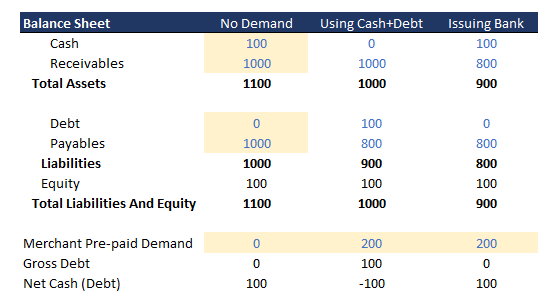

Unlike most companies, acquirers deploy massive capital into the pre-payment business. As a result, the reported balance sheet and the actual figures for cash and debt may diverge.

When an acquirer receives a demand to prepay money from merchants, it could use proprietary cash, issuing banks, or debt.

However, as the image above shows, the balance sheet doesn’t show the real impact when an acquiring company issues a bank for the pre-payment.

Keep reading with a 7-day free trial

Subscribe to Giro's Newsletter to keep reading this post and get 7 days of free access to the full post archives.