Brazilian Banks

Brazilian Banks

Outlook for 2022 and 4Q21 wrap-up

Disclosure: All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing/gambling your money.

(14 minutes read)

Access to Interactive Model.

Outlook for Brazilian Banks

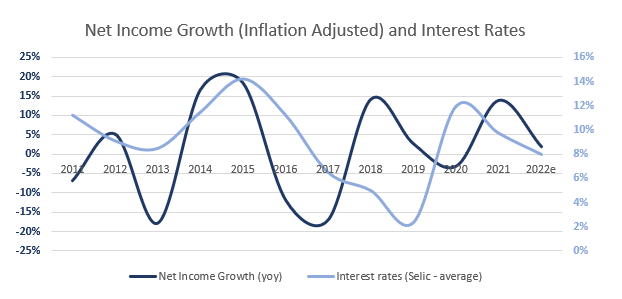

The large banks listed on the stock exchange showed decent results throughout the year, mainly benefiting from a normalization of provisions levels.

While higher interest rates tend to benefit NIMs for most banks, there are risks from weaker GDP growth and high inflation, which can pressure loan growth and deteriorate asset quality.

Brazilian banks have been among the worst-performing banks globally. On the other hand, most banks globally have risen in the last 12 months, with only Turkish banks declining more than LatAm banks. This is partly due to the region’s challenging macro and political environments.

In particular, Brazil will face high single-digit inflation throughout this year, 1% GDP growth, and an election to go through.

Although many economists are writing that Brazil hit the peaked its tightening cycle, there is a huge question mark regarding populism and commodities prices that might put pressure on the Brazilian Central Bank (“BCB”).

Consequently, the expectations for 2022 for Brazilians Banks are tailwinds from higher rates but much more pressure for passing through spreads and worst asset quality.

To illustrate, consider a basket with ITUB 0.00%↑ , BBD 0.00%↑ , and BBAS. In real terms, I’m expecting a 1,7% earnings growth, above its 1,3% average, though it’s inferior to previous tightening cycles.

If you think this is too conservative, keep in mind that last year’s inflation was ~8%, and 2022 will not be much different. Also, given that average rates should be above 10%, Brazilian Banks should have less headwind hitting earnings growth.

I’m expecting a flat year-over-year inflation-adjusted growth for NII and Fee revenue. But, honestly, that sounds aggressive considering the pressure on margins on inflationary cycles.

Therefore, we should have a decent year for dividend and buyback, with nominal growth above 10%, almost 2% in real terms.

Curiosity: In the past 12 years, the CAGR for dividends and buybacks in real terms barely hit 2%, another indicator that the industry is mature.

Furthermore, I carried out some exercises to assess the internal rate of return for those equities, considering the estimates presented.

First, it is essential to remember that the long-term return is the sum of the change in book value, distributed earnings, and any expansion/contraction in the traded multiples.

Instead of using the net income, an alternative to evaluate value generation is calculating the YoY change in the BVPS (Book Value per Share) and increasing the distributed earnings.

I understand this metric as the effective generation of value for the company’s shareholder, as it reflects the accumulated wealth (change in equity value) and distributed (earnings) by each asset unit (number of shares outstanding).

One way to interpret the table above is that Banco do Brasil will generate in 2022 a gain of R$3.4 in equity value per share and distribute R$5.2 per share in dividends, a Total Return of R$8.6 for the shareholder.

Thus, keeping the multiples constant, if this stock is being traded at R$30 reais, the implicit Total Return to Mkt Cap is 28.6% (8.6 / 30).

The image above is the wealth generation history divided by the company’s market value. It reflects a lot of what we commented on earlier.

By presenting the best guidance and not having a significant appreciation after the quarter’s results, ITUB’s implicit return increased, even though its shares were also appreciated.

Also, Banco do Brasil, despite increasing more than 10% after disclosing the quarter’s results, continues to be the bank that offers the highest rate of return if it comes to delivering the guidance.

On the other hand, despite suffering sharp drops after the quarterly results, BBDC remains the bank with the lowest expected value generation for 2022 due to lack of execution.

Bradesco ($BBD)

Bradesco was the first bank reporting this earnings season, startling the market with weaker than expected 4Q21 numbers.

Earnings came 5% short of the Street at R$6.6bn, even though the “lower quality” market NII did well. Meanwhile, BBD printed R$3,2bn GAAP earnings, impacted by a R$1,9bn reclassification.

The TVM includes results from the reclassification of securities in the portfolio from “Available for Sale” to “Trading” and turnover in the financial instruments market (MTM).

Also, $BBD reported weak guidance for 2022, with client NII growing less than loan growth and OPEX pressuring the bottom line.

Obviously, the earnings miss plus disappointing guidance are responsible for the poor relative performance versus peers.

Furthermore, BBD’s ROE has been showing a deterioration dynamic, bringing questions about management execution since the spread between “recurring” earnings and cash earnings hit an all-time high.

Curiosity: Banks report a Pro Forma and a BRGAAP income statement. In the Pro Forma, management has greater “flexibility” to classify revenues and expenses. So, usually, there is a gap between those earnings, which we should pay close attention to.

Itaú ($ITUB)

After BBD presented results below expectations with equally timid guidance for 2022, the market was apprehensive about the banks’ results.

Therefore, it was a relief to see the quarterly result (and guidance) of ITUB, which was very strong and with better trends than Bradesco’s.

The main highlight was the guidance for 2022, which indicates a solid customer margin, maintaining the margin of 4Q21 throughout 2022.

Furthermore, even with PDD guidance indicating strong growth (>30%), a coverage level more or less similar to what we saw in 2021 seems to be implied.

Though ITUB doesn’t present guidance for net earnings, the implied by the guidance is between R$26.1 and R$34.5 billion (I haveR$30,5bn), with an ROE slightly above 20%.

Therefore, if we choose the average of the estimates provided to the market, ITUB intends to deliver a result ~5% above expectations for 2022.

Banco do Brasil ($BDORY)

Once again, Banco do Brasil (“BBAS”) reported net income exceeded all market estimates. On the positive side, even adjusting these lines as “non-recurring,” BBAS would still have presented a net result above the market’s expectations, led by the expansion of the loan portfolio.

Nevertheless, on the negative side, most of the above-expected gains came from lower provisioning and non-recurring gains related to PREVI.

Given the lower level of provisioning in 2Q21 and the treasury gains in 3Q21 that caused positive non-recurring effects on BBAS’ earnings, we believe that the market was expecting some kind of “normalization” in 4Q21.

In addition, another highlight of the result was the result guidance for 2022, which is above (>15%) what the market expected. During the earnings call, some things caught our attention.

Asset quality should be maintained throughout 2022, with a slight reduction in the bank’s coverage ratio. We see this sign with good eyes, given that the BBAS coverage ratio is at 325% versus 248% for the Financial System National.

New initiatives in customer service models investments should generate a higher-than-expected growth in corporate expenses. However, even if the news is not favorable, the increase in costs is more than offset by expanding the business’s revenue lines.

NII should improve in terms of assets (volume, mix) and liabilities (savings and judicial deposits), with a good expansion of the expanded portfolio throughout the year. However, at this point, we see that there may be a slight downside risk in the numbers, given that the institutions’ repricing capacity may end up being insufficient with the increase in the cost of funding.

BBAS comes from a sequence of very robust results, delivering growth and profitability. Perhaps, the market is apprehensive of sequential beating on non-recurring, but the operational improvements are — indeed— notorious.

Also, BBAS built a huge cushion throughout 2019 and 2020, boosting its coverage ratio to ~1,4x the Financial System National’s average. So it wouldn’t surprise more beatings on non-recurring along the following quarters.

Therefore, if management delivers the guidance, the shares will negotiate a P/E level for the end of 2022 close to 4x, with an EPS CAGR (nominal) >10%.