Food for Thought #5

Food for Thought #5

Edge of the chasm; Two sides of the same coin; Breakout week; $NU, $STNE, $MELI, and much more.

(10 minutes read, 14 pages)

Today’s outline

Edge of the chasm

Two sides of the same coin

Breakout week

In case you missed it ($MELI, $STNE, $NU)

Portfolio (PRO)

Watchlist (PRO)

Brazilian Banks ($BBD, $BDORY, $ITUB) (PRO)

Making money with elections in Brazil (PRO)

Short Populism (PRO)

Links to Interactive Models (PRO)

Stone ($STNE), Petrobras ($PBR), 3R (BVMF: RRRP3), Sinqia (BVMF:SQIA3)

Edge of the chasm

On Tuesday, BofA released its Global Fund Manager Survey, a claimed report for identifying market sentiment and global trends.

Investors continue to see hawkish central banks, inflation, and asset bubbles as their main concerns. In addition, they continue expecting EM equities and Oil to outperform in 2022.

Nevertheless, the chart above caught my attention, which shows yield curve flattening expectations have increased, reaching extreme levels seen only a few times in the past two decades.

A flat yield curve is an indication that investors are worried about the macroeconomic outlook. A few reasons the yield curve may flatten is market may be expecting inflation to decrease, lower growth, or the FED to raise the federal funds rate (“FFR”) in the near term.

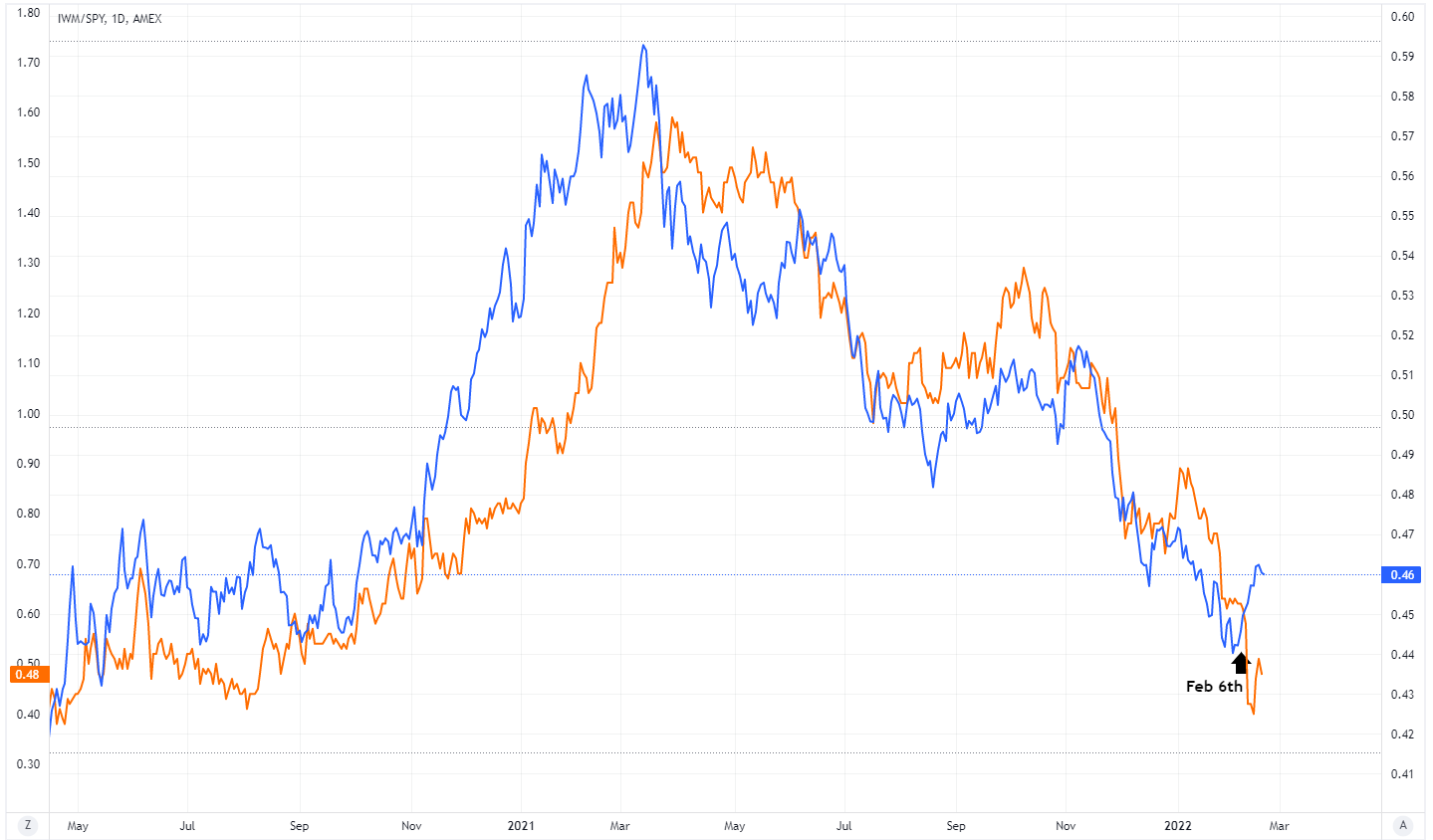

Two sides of the same coin

From a fundamental perspective, the Russel 2000 small-cap index is composed of cyclical small-cap companies and shows signs of growing weakness.

Since November, the bottom-up consensus forecast for Russell 2k profit margins dropped 4p.p. in 2022. Also, roughly a third of Russell 2k stocks should report negative net income over the next twelve months.

Also, the spread between 10yr and 2yrs maturity USTs has confirmed the lower growth environment trend, pricing lower growth ahead.

Affected by lower growth expectations, the Russell 2000 also contains stocks popular with US retail investors, which tend to hold tech and small-cap stocks, have been weakening breath since 2021.

Although sentiment toward commodity and other value companies has been increasing since September of 2021, the companies representing these sectors in the Russell 2000 have been lagging Large Caps.

Baskets with higher exposure from retail investors have been suffering inflationary pressure on valuations, lower growth expectations, and aggressive retail outflow from equities — tech allocation fell to the lowest level since August 2006. We like that.

Since you’ve been reading my stuff for more than a month, why don’t you redeem a free trial?

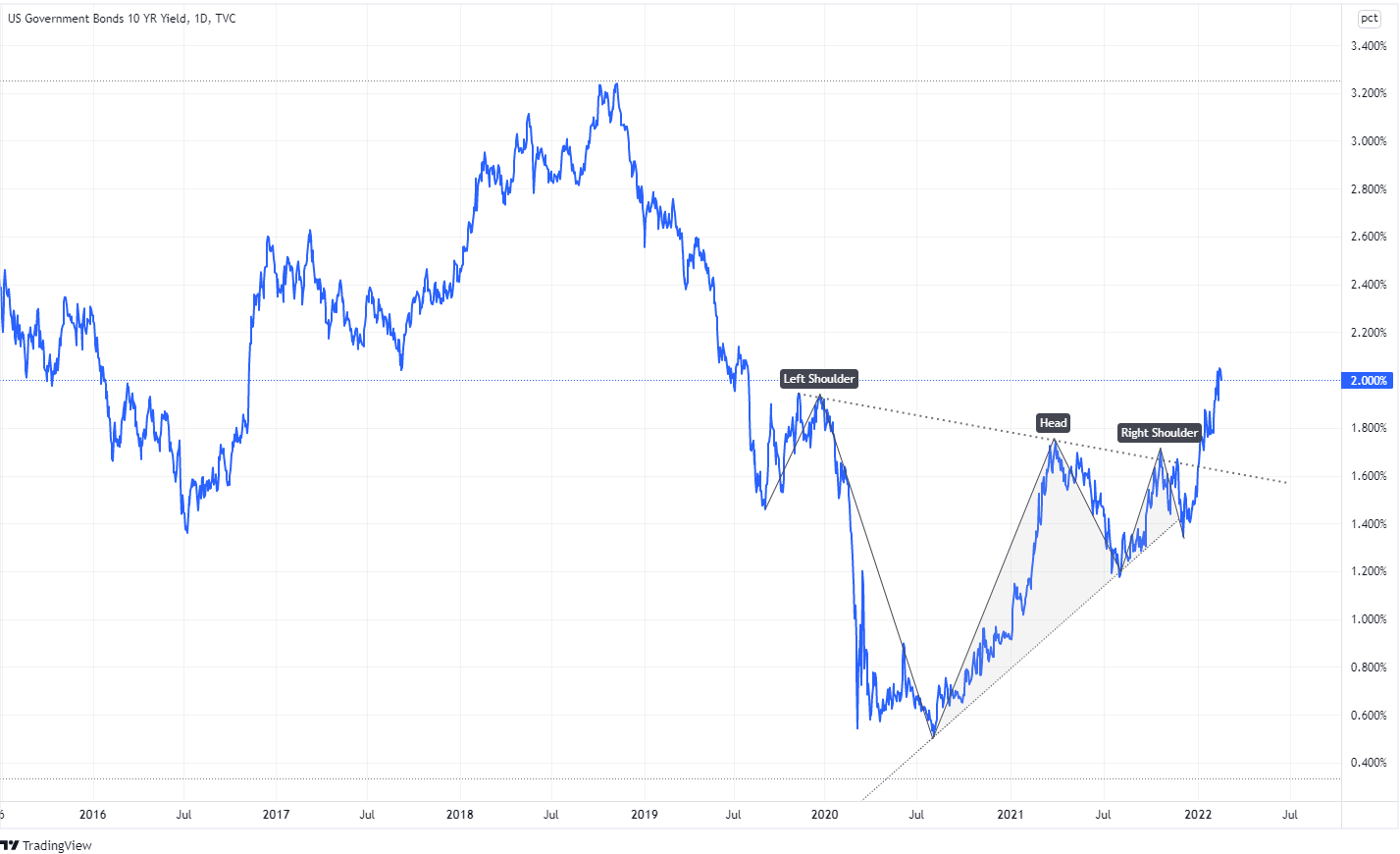

Breakout Week

I’ve been writing a lot about the steady advance in commodities sectors, and they may (continue) be the most critical development in the financial markets.

My favorite sector as a proxy for implicit inflation is metals and mining. Recent events, such as easing policies in China to stimulate demand and US data, might have led to the next leg-higher for the sector.

The second piece of evidence contributing to this thesis is the serial breakout in the bond markets (Japan, Germany, US,…) that soared through the past couple of weeks.

Finally, the last breakout of the week I’m using as evidence to my bull thesis on XME is Brent, who broke a 12-years falling wedge. Also, the bull thesis for Oil continues to play out, as we vastly discussed over the past weeks.

In case you missed it ($MELI, $STNE, $NU)

$MELI

$STNE

$NU

PRO Content

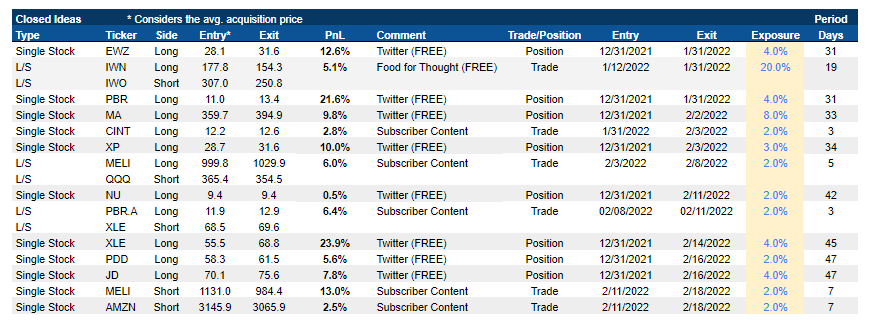

Closed Ideas in 2022

Keep reading with a 7-day free trial

Subscribe to Giro's Newsletter to keep reading this post and get 7 days of free access to the full post archives.