Model Updates

Model Updates

Stone ($STNE) and Sinqia (BVMF: SQIA3)

We are updating our models for Stone and Sinqia following 4Q21, incorporating management’s guidance for STNE 0.00%↑ and better than expected trends for Sinqia’s operations.

Stone

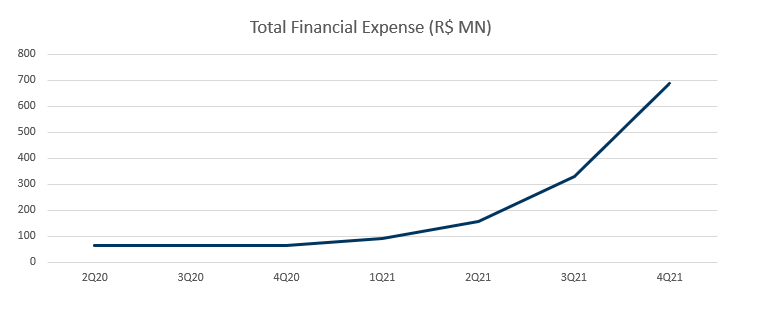

In the 4Q21, overall results surprised the upside on revenues ~9,5% above GIROe, but very high expenses ~23% above GIROe drove the miss.

Specifically, Opex was impacted by increased costs related to TAG, personnel/ S&M expenses, cloud expenses, investments in technology, and customer support.

Also, financial expenses continue to soar, reaching as much as R$688m in the 4Q21, up from R$331m in 3Q21 and R$64m in 4Q20, impacted by higher working capital needs related to the pre-payment of receivables.

Management mentioned that the take rate was increased to 2.02% in January 2022, bringing a new question if there is space for expanding the take rates.

So, the overall changes considered i) industry growth above expectation, ii) higher funding cost and take rate, and iii) higher churn.

Since 2020, the industry’s growth has been fueled by a massive transaction from cash transactions to cards, digital wallets, and instant payments, such as Pix.

So, in the past weeks, we spent a lot of time researching and developing a new model for estimating payments’ total addressable market (“TAM”) that considers recent trends in the payment industry.

First, for 2022, we reviewed our Card Expenditure from R$2,803bn to R$3,263bn (+16%). Second, we incorporated higher financial expenses led by higher than expected Brazilian Federal Fund Rates (“Selic”). The illustration below summarizes the changes.

Keep reading with a 7-day free trial

Subscribe to Giro's Newsletter to keep reading this post and get 7 days of free access to the full post archives.