New guideline for Fintechs in Brazil

New guideline for Fintechs in Brazil

Daily Crunch #5

Disclosure

All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing your money. Giro’s Newsletter makes no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in the piece. Any assumptions, opinions, and estimates expressed in the article constitute the author’s judgments as of the date hereof and are subject to change without notice. Any projections contained in the information are based on several assumptions about market conditions, and there can be no guarantee that any projected outcomes will be achieved. Giro’s Newsletter does not accept any liability for any direct, consequential, or other loss arising from reliance on the contents of this presentation. Giro’s Newsletter is not acting as your financial, legal, accounting, tax, or other adviser or in any fiduciary capacity.

(8 minutes read)

Hi.

The Brazilian Central Bank (“BCB”) released a guideline (only available in Portuguese) on new capital regulation for the Brazilian fintechs.

The new approach requires more capital for large fintechs than the smaller companies, and in the case of the credit card business of large fintechs, the new regulation will use a similar approach to BIS standards. The implementation will happen in tranches from 2023 to 2025.

We went through Resolution 4.657/18 in Sinqia’s post, in which the BCB increased the number of fintechs upon their approval.

According to the legislation, authorized fintech can act in two ways: i) as a direct credit company (“SCD”) or ii) as a loan company between people (“SEP”). The first allows credit operations with its resources, while the second enables credit operations between people, known as peer-to-peer lending.

In 2018, the BCB issued Circular No. 3.885, which provided new payment companies rules (“IP”). Most listed Brazilian fintechs operate using these licenses, though they’re recognized as “banks.”

Furthermore, the companies are reporting in a Prudential Conglomerates and Financial Institutions according to Resolution 4.280/13 — articles 1 and 4 —, where each of them could operate a different license in a separate subsidiary under a Conglomerate (if any).

For instance, Nu operates its IP through the Nu Pagamento subsidiary, the IF through Nu Financeira, and Broker through Nu Invest. They are pieces of the conglomerate called Nubank.

The capital requirement for an IP is defined as the higher of i) 2% of the average monthly payment volume of the last 12 months; and ii) the balance of electronic currencies (BCB No. 3.681/13).

The capital requirements for an IF are similar to those for banks. For example, in the case of Nu Financeira, the minimum capital is 14% until 2022, vs. 10.5% for banks).

An IF has some limitations in terms of funding, as it cannot receive demand deposits or savings. However, they can issue specific types of deposits, such as RDB “Recibo de Depósito Bancário” (which is very similar to a time deposit for clients).

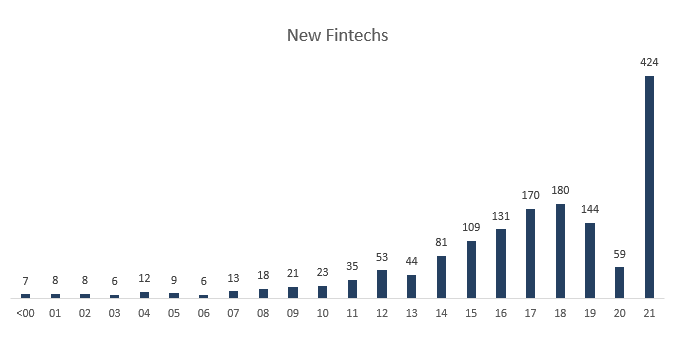

In my opinion, the BCB created a huge arbitrage for companies to ask for an IP license since the required capital is ridiculous (versus BIS). Probably, this was the biggest trigger for new Fintechs to come to the market.

For instance, in the last few years alone, 977 new Fintechs were opened, compared to just over 1,000 in the remaining balance of the sample.

The BCB labeled the financial institutions in three main groups:

Financial conglomerates led by financial institutions;

Payment companies (IP) not linked to other financial institutions;

Payment companies (IP) related to other financial institutions (IF).

Most of the large fintechs (like Nubank and Meli) will be classified in the third group as they have the payment company (that holds their credit card business) and the non-banking financial institution (IF).

Group 3 will now have a similar capital approach for their credit card business as the banks. However, note that the detailed risk-weighted factor used in their credit card business was not yet published.

But since Nu is not licensed as a bank, the company’s risk-weighted asset (RWA) density (RWA over loans) is much smaller than other players, and the BCB indicates that the RWA density gap will close over time.

Right now, I’m crunching a few numbers, but regulatory changes will hit all Fintechs that are not operating under a banking license. Should post about it in the following days.

At Giro’s Newsletter, readers are the boss. This Friday, I’ll interview Sinqia’s CTO, Mr.Thiago Saldanha. Sinqia is the most significant infrastructure provider for financial institutions in Brazil, including for PIX.

I’m sure Mr. Saldanha will help us deal with the hard questions. If you got any, send me a DM on Twitter. I’ll be pleased to address your matter. So make sure to subscribe and share it. This is the best thermometer to set a direction for my posts.