$SE 4Q21

Disclosure: All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing/gambling your money.

Going through Sea Limited ("SE")'s earnings, I'd say management is confident with their strategy given the downward trend they showed this quarter.

Sea reported 4Q21 revenue of $3,2bn (+106% YoY), 12% above Consensus. Adj EBITDA loss of -US$492mn was higher than -$168mn Consensus, on higher losses in both e-commerce and other segments (food delivery). Net loss was -$618mn, in-line with the Consensus of -$618mn/-$653mn.

Gaming: Bookings came in at $1,1bn, 10% below my estimates. This was mainly driven by weaker than expected QAU growth/pay ratio trends. Remarkably, its QAU decreased by 10% QoQ while its QPU decreased by 17%. EBITDA margins also missed our expectation at 55,7% vs. ~60% from Consensus, given higher than expected cost of revenue and marketing expenses.

Management commented that they are facing headwinds from reopening and that many gaming markets are seeing fast reversal trends in recent months.

On weaker margins, management remarks that they have been investing in further bolstering its franchise and channel, including videos, music, and game development. Consequently, sales and marketing expenses and R&D have increased. Also, they're looking for more partnerships to increase loyalty.

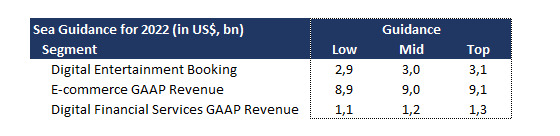

Guidance - Bookings to be between US$2,9 - US$3,1bn. The guidance considers these headwind factors from reopening and India impact but is MUCH lower than Consensus ~$5bn. I wrote about India's impact before:

Given the breakdown between India and business' headwinds, it's harder to read the guidance, but the latter is a huge hit. As a result, the midpoint will be close to 2020 levels.

E-commerce: Total GMV grew 52,7% YoY to $18,2bn (vs Consensus of $19,2bn). Revenue was $1,6bn for 4Q21 (+10% QoQ). Sales and marketing as % of GMV was 4,6%, above 3Q21 and 4Q20. As a result, adjusted EBITDA loss of -US$878mn is much higher than Consensus.

Management commented that Shopee is on track to reach positive EBITDA in ASEAN and Taiwan this year, as they continue to see improvements in unit economics. For the management, breakeven can be achieved through higher take rates and better cost efficiency (scale).

Management remarks that they'll use the $7bn proceeds they raised last year for front-loaded investment in Shopee and SeaMoney. By 2022, Shopee LatAm (especially Brazil) will be the core focus of investment; investments are generally front-loaded, but unit economics will improve with scale.

Guidance - Revenues to be between $8,9 - $9,1bn (Consensus of $8,6bn). Management expects to see its take rate increase to low teens in 2022. Take rate increases will be seen across all types (advertisement, commission, and logistics-related activities).

Fintech: SE continued to see strong uptake of its fintech offerings, with e-wallet TPV reaching US$5,0bn in 4Q21. Revenue rose 49% QoQ to $198mn, supported by lending business. Also, loans receivables are now more than $1,5bn in 4Q21.

Management provided guidance for the segment for the first time with revenues between US$1,1 and US$1,3bn (Consensus: $870mn).

All in, the Gaming segment showed a downward trend that requires more reading/studying to better understand its dynamics.

The guidance for the commerce segment and management's comments imply greater investment in LatAm, which should increase SE's sales and marketing expenses throughout the year.

In the following section, we're gonna have fun crunching a few numbers.

Is it possible that Shopee will hit the breakeven for ASEAN + Taiwan?

Yes. Although we don't have the breakdown for location, we can assess Sea's consolidated PnL per GMV.

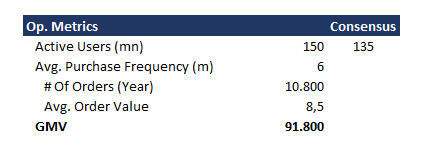

First, to estimate the GMV, we considered the monthly average user in 150 million, with an $8,5 average order value to reach out to $91,8 billion in GMV.

Then, we considered the consolidated cost/OPEX per GMV to estimate the average Ebit for GMV Shopee has. Considering that LatAm's higher sales and marketing expenses should be polluting the estimates, it looks reasonable to Shopee to achieve breakeven throughout the year.

Is it possible that Shopee will perform better than local players in Brazil?

Yes. Considering that the TAM in Brazil will grow at a 20% pace through the next five years and fixating the CAC (inflation-only), Shopee can take a lot of market share in Brazil.

However, the premises might be too optimistic. First, eventually, Shopee will have to halt subsidies to become profitable in the region.

Second, Shopee would have to invest heavily in service level (app, wallet, credit,…). Also, higher service level investment should be funded by resources destined to the region, slowing its growth.

So far, Shopee doesn't look to be capturing Meli's market share, nor the 1P from durable goods from traditional players. But nevertheless, it's a player that cannot be ignored.