Shopee Brazil

Disclosure: All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing/gambling your money.

Last update on 2022/03/04

Hi.

A lot is being said about Shopee in Brazil, especially how Sea will capture a lot of market share throughout the following years.

I posted briefly on Sea’s earnings yesterday and shared my view about management comments during the conference call.

Though the post is a good wrap-up on earnings, it doesn’t really answer pivotal questions, such as if SE 0.00%↑ will be able to capture so much market share or not. So I decided to write a second post to address these matters.

Before, an observation: I’m writing a post on MercadoLibre (“Meli”) to paid subscribers, so I’ll not be sharing details on unit cost estimates for MELI 0.00%↑ since that would be unfair with paid subscribers.

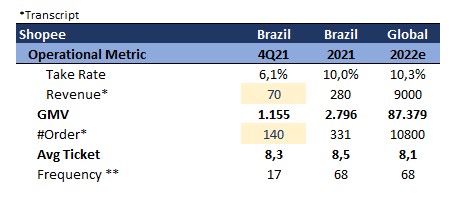

With that said, the image above is my picture for Shopee’s operations in Brazil and Global. For Brazil in 2022, I pretty much annualized the operational figures that management disclosed along with the earnings call in Brazil.

It’s important to highlight that management stated that Shopee will reach operational breakeven throughout 2022. Also, management explicitly pointed to ASEAN + Taiwan operations, not the Global.

Nevertheless, it’s been widespread to see analysts assuming that Sea will reach breakeven for Shopee Brazil as well, which a profoundly disagree.

Shopee’s operations in Brazil are very early stage, with a lot of costs, expenses, and shipping subsidies to be diluted, a take rate to be increased before talking on breakeven.

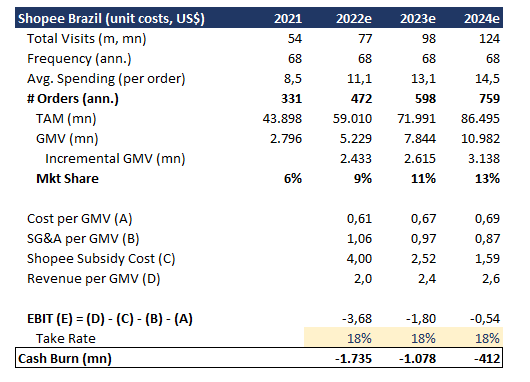

Garena has been an essential component of funding commerce growth in the past years. However, with disappointing figures expected for the following years, Shopee Brazil would rely on the $7bn Sea raised last year.

To achieve breakeven in Brazil, Sea would have to ramp up its operations faster than they’ve ever done before. So, considering that they generate an incremental $4bn in GMV, that could be resumed in a $1,8bn cash burn.

However, if Sea archives operational breakeven for ASEAN + Taiwan -- I believe they will --, they might start looking for different monetizing routes in Brazil, such as SeaMoney.

As Sea, for being listed outside of Brazil, the cost of equity for Sea to raise money and start offering credit products in Brazil has an outstanding value proposition.

In that case, Sea would have to prioritize resources, capture enough market share to achieve a viable scale, and start developing different solutions.

Therefore, independently of the direction a look, though Sea has incredible growth potential in Brazil, they still have a long and tortuous way to go until they reach profitability in Brazil.