Sinqia (BVMF: SQIA3)

Sinqia (BVMF: SQIA3)

Leading software provider for the financial industry

Today’s Outline

Tearsheet

What is SaaS?

Revenue sources

New organic growth avenue

Next steps

Inorganic growth

M&A Process

Why do M&A?

Risks

Equity shareholder dilution

Valuation

Sinqia stand-alone model

Monte Carlo Model

Introduction to Sinqia

Sinqia is a leader in software development for the financial sector in Brazil. In addition to exposure to the financial and technology industries, the company has a well-defined strategy, good management, decent governance standards, with growth and profitability.

The company's revenue comes from its software and services business. Within the software, Sinqia operates in the pillars of banks, pensions, funds, and consortiums, providing services to more than 350 financial institutions through lasting relationships.

The Central Bank has been conducting a significant regulatory change process to encourage greater competitiveness among financial institutions in recent years.

As a result, the search for companies capable of offering the necessary infrastructure to operate has been growing at an accelerated rate.

There are two ways to provide these services. The first is through license development and sale, where the company receives a large portion of the payment on implementation and then smaller amounts throughout maintenance contracts.

The first model, licensing, involves a significant cost of personnel to implement, customize and repair the solution. In addition, it isn't easy to scale because of customization and the extensive implementation process, which can take months.

In the second model, the company offers the same interface to the customers of that product. Besides paying for a smaller implementation, the customer starts paying a monthly fee to use the product.

Sinqia is switching from the first model to the second, offering a less customizable solution, easy to integrate that provides superior profitability.

Beyond that, the company has developed a superior strategy for its inorganic growth, acquiring competitors for years and pilling up revenue at attractive valuations.

What is SaaS?

The model was created 20 years ago by Marc Benioff, founder of Salesforce. The idea was to create a collaborative network between users. Then, when one encounters a particular problem, the solution is quickly implemented, benefiting all users.

For example, SuccessFactors, HR management software acquired by SAP, which is used by GE — known worldwide for having an excellent HR team and team management.

By using SuccessFactors, in the end, the software owner ends up getting insights from the GE HR team on platform improvements that affect the entire system.

This architectural style with centralized applications serving multiple clients is known as multi-tenancy. In the cloud (cloud server) era, it is possible to vertically integrate and create incredible businesses with much higher barriers to entry. Once you reach a particular scale, it is very complex for new entrants to establish themselves.

SaaS ends up bringing two significant benefits: i) deflationary tariffs, preventing new competitors from entering the market when a particular scale is reached, and ii) the margins that mature companies achieve are phenomenal.

Deflationary tariffs and a higher gross margin translate into the more significant potential for investment in the solution and cash generation for shareholders.

In Sinqia's case, the migration of all platforms and customers to SaaS should expand the company's gross margin and greater financial power in developing new market solutions.

Finally, we estimate that the migration process will continue until 2025, when Sinqia will be running its clients in a centralized solution, easy to scale and lower the cost of serving.

Revenue sources

Since its IPO, Sinqia has transformed itself into a one-stop-shop of services for companies in the financial sector, offering products and services through its software and services verticals. The software pillar serves banks, pensions, consortia, and funds.

Sinqia's product shelf results from investment in R&D and acquisitions made throughout its history. In the coming years, we expect Sinqia to continue on its leadership trajectory as a software provider for financial institutions, especially after the regulatory changes carried out by the Central Bank.

On the other hand, the service division underwent an intense transformation process. Before, the primary source of revenue came from outsourcing, which was mainly the service related to the implementation and maintenance of a specific product license.

However, after understanding that it needed to change its business model to SaaS and with the regulatory change, which we will discuss in more detail later, Sinqia started to focus on offering digital transformation and consulting services.

In addition to consulting having a relatively higher ticket than outsourcing, developing a solution for a specific client can lead to improvements and new products.

The most significant competitive advantage of Sinqia's consulting and transformation team is the autonomy that the board has achieved over the years.

For example, if a customer agrees to pay, the company may have a more aggressive attraction and retention program than the software industry.

This has been translating into greater customer satisfaction and significant increases in the prices charged by consulting firms.

Since you’ve received my stuff since last year, why don’t you redeem a free trial coupon?

New organic growth avenue

In 2018, with Resolution 4,657/18, the Central Bank increased the number of financial institutions considering some fintech upon their approval.

According to the legislation, authorized fintech can act in two ways: i) as a direct credit company (SCD) or ii) as a loan company between people (SEP). The first allows credit operations with its resources, while the second enables credit operations between people, known as peer-to-peer lending.

Also, in 2018, the Central Bank issued Circular No. 3,885, which provided for new rules for Payment Institutions (IP). More than ever, it is essential to reduce costs to remain competitive; it is necessary to rely on process automation.

In addition, the Central Bank continues to show commitment to changes that allow for a more competitive environment among companies. Therefore, we highlight in the coming years:

Open Banking Regulation: Before the regulatory change, customer identification data belonged to the financial institution, so other institutions could not see whether such a customer was a good payer or not.

Open Banking creates a shared communication interface (known as an API), which allows other companies to access user data in different institutions — as long as they are previously authorized.

With the information in the hands of the customers, there is an increase in the offer of credit from different institutions to the customer. The new institutions will function as a credit supply frontend, originating credit with another organization carrying the risk on the balance sheet.

This format is more efficient because the wholesaler (a large institution that offers credit) does its customer risk assessment, incurring no risk of the frontend pricing the bad credit.

The originator can also grant the credit using its capital or sell the portfolio to a FIDC. Again, the objective is to increase the offer of credit to the final customer without increasing the risk of the system.

Instant Payment - PIX: The significant penetration of smartphones and QR Codes in the global market and especially in China has been opening up more and more space and infrastructure for the democratization of instant payments, which aims to facilitate transactions and reduce fees.

Launched by the Central Bank in February 2020, PIX is a new system that facilitates the transfer of values between people, slips, and even tax collection. With PIX, the system will be up and running 24/7, executing transactions in seconds.

PIX's primary role will be to attack cash and debit transactions. However, the impact on credit transactions is not yet conclusive.

Marco Legal das Startups: Bill that came into force on August 31, 2021, which brings a series of facilities to open a technology company, offering greater legal certainty to investors in the early stages of the business, through a new corporate model: simplified corporation. The great advantage will be the increase in the level of legal certainty for attracting capital from third parties.

Regulatory Sandbox: Structure created by the regulator that allows small tests in the financial sector, in a controlled environment, and on a small scale. The program is expected to scale the industry's level of innovation exponentially, allowing companies to start testing new processes and tools at a lower cost.

The regulatory changes already made, added to the pipeline for the next few years, confirm the regulator's reformist agenda, which should sustain the increase in new entrants and innovations in the industry.

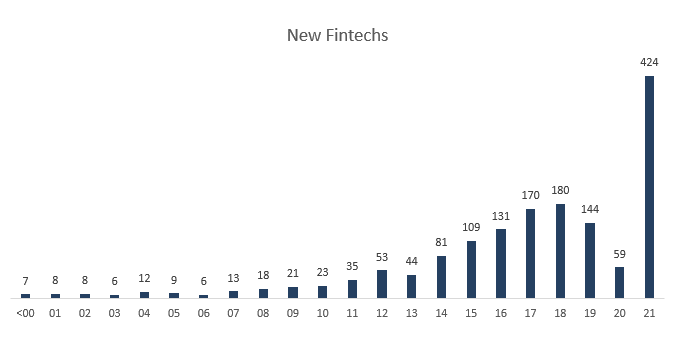

According to Fintech Lab, we ended 2019 with more than 700 fintech, of which 49.6% were born in the last four years. Moreover, of all the capital invested in startups last year, a third went to Fintechs, mainly digital services and credit.

The chart above is an incredible portrait of the fintech opening market in Brazil. In the last few years alone, 977 new Fintechs were opened, compared to just over 1,000 in the remaining balance of the sample.

Watching ABES and AB Fintech participants, we believe that more than 80% of fintech are considered Micro or Small companies, with revenues of up to R$3.6 million per year, with abundant access to capital, even among the smallest of them.

In addition, according to the Central Bank, since it announced the rules that deal with the regulation of credit fintech in Brazil, it has already authorized 30 of them, 24 Direct Credit Societies (SCD) and 6 Loan Societies between Persons (SEP). ).

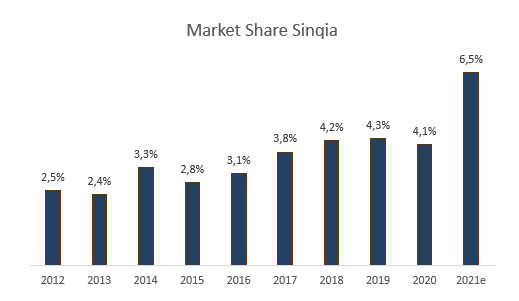

Looking at the competition, it is inevitable that the increase in the number of companies and capital invested will also increase the technology used in the solutions. That's where we highlight Sinqia's performance, accelerating its consolidation process in the market.

Even with an estimated market share of just over 6%, it stands out within a market dominated by small service providers and some companies with some muscle but without offering the full range of products and services.

One characteristic that has emerged in recent years, which was not present before the regulatory change, is the demand for service providers with time to market. Every day, it becomes more critical for the service provider to adapt their product/service to resolutions and standards.

Next steps

To benefit from the industry's growth, the company operates under four pillars: i) organic growth through the capture of new customers; ii) the development of new solutions; iii) cross-selling products, taking advantage of new possibilities in the base itself and iv) acquisitions.

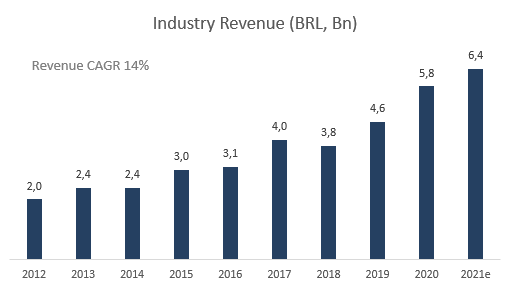

From an industry perspective, according to ABES, the market for software providers for financial institutions has been growing consistently, with an apparent acceleration after the regulatory changes that we mentioned earlier.

When we look at cross-selling and up-selling, we see two points of action that will help drive growth. First, the company is moving its legacy customer base to the cloud.

This takes time, effort, and capital, as churn during the transition period is higher. In addition, as Sinqia is a company that traditionally makes a lot of acquisitions, some verticals still do not have a single product for all customers, as is the case with pension plans.

Consequently, the vertical's gross margin is lower than others ahead in migration and consolidation of the portfolio operating in a single product.

In addition to the company migrating to the SaaS model, with recurring revenues, the low change in software providers is another characteristic of the financial vertical.

Because the implementation is complex, training and product adaptation are long and slow. In addition to the software being "mission-critical," changing suppliers is rare. This implies a churn rate of 3% p.a., which translates into customer relationships exceeding 30 years.

There is another less intuitive angle for changing suppliers to be less frequent, which is career risk. There is no incentive for a manager to change his software vendor; on the contrary, as it is a complex, expensive, and slow process, switching suppliers is risky from an operational and career point of view, leading the current supplier to a "status quo" condition.

As mentioned earlier, we believe that there is potential for new customers in payment institutions, credit companies, digital banks, in addition to the possibility of entering the investment management segments and other emerging technologies.

Last but not least, the previous growth strand for Sinqia is M&A. To understand what Sinqia will look like five years into the future, we will divide the company's history into three periods:

Phase I (2004-2012): Company receives a contribution from the Private Equity Stratus and a loan from BNDES, totaling R$7 million, to finance a cycle of five acquisitions, leading to a 10x increase in revenue in the period.

Phase II (2013-2019): Company makes its IPO and receives a new loan, totaling R$90 million, to finance the next round of growth through nine acquisitions, multiplying sales volume by 3x in the period.

Phase III (2020-2025): Company raised BRL 362 million in September 2019, an offering of BRL 250 million in debentures, and, in September 2021, a new offering of shares of BRL 400 million to finance its third and more extended growth phase.

Since the beginning of Phase III, the company has already made more than nine acquisitions. As a result, we estimate that the company still has a purchasing power of between R$100m and R$200m, considering that there would still be Capex with the purchase of Simply, Lote 45, and QuiteJá.

Furthermore, it is essential to observe the acquisitions of this last phase, especially Simply, FEP, QuiteJá, and Lote 45. At first glance, the impression may be that Sinqia paid dearly for the companies, but this is not the case.

Unlike other acquisitions, these companies offer a 100% cloud-integrated solution, with very high scalability, a fast customer onboarding process, and no dependency on the legacy.

This translates into higher margins and greater scalability for these companies. Simply, for example, performs the onboarding process (registration) of clients in institutions such as C6 and Banco Inter. Regardless of whether the customer consumes the financial product, the company's revenue comes from registering the registration request.

In addition, because the solution was born in the cloud and does not depend on legacy servers, its scalability with a low degree of friction is far superior to other market offerings.

M&A Process

We believe that a few hundred companies are ripe for acquisition, many with the same profile as Sinqia itself: former protagonists of the great automation process of financial institutions decided to undertake and have the opportunity to sell their business.

We highlight here the two types of sellers: i) those who wish to retire and find a possibility to sell their customer base; or ii) young entrepreneurs who see scale limitations in their businesses and the possibility of growing even more by being acquired.

Most of the acquisitions made by Sinqia in recent years have been in format (i), with mature portfolios and long-term customers. However, as we have already mentioned, the mix started to have more case (ii) components, mainly in emerging technology companies.

For case (ii), the gain in scale comes through the commercial access that Sinqia allows. For example, as Sinqia supplies software to Bradesco, Simply's offer automatically becomes a new product on the shelf, as Simply did not reach this customer before.

As we have already mentioned, although the solution is more remarkable, individual conflicts of interest, such as career risk, works as an entry barrier for smaller companies.

On Sinqia's side, the biggest gain from acquisitions is horizontal, adding new products to the shelf and accelerating organic growth and operating margin expansion.

The collaborative environment is crucial to success. For example, for acquired companies, Sinqia's access to and expertise in larger trading is unique, unlocking growth that Fintech alone could not achieve.

For Sinqia, more than buying a new scalable and profitable product, it is managing to bring the founding partners of these companies into Sinqia. As a result, in addition to managing their specific products, Sinqia’s corporate culture is also improved.

The acquisitions made over the last three years should generate long-term benefits for the company in the long run. They are entrepreneurs who managed to create scalable solutions within a highly competitive market and take more time to market for Sinqia in the solutions developed.

Why do M&A?

For a good reason, many investors tend to avoid companies that carry out many M&A processes. The main reason is that acquiring companies is easy to add revenue, but it's also just as simple to destroy value during the onboarding process.

Many M&A think about cost synergy, but little about the complementarity of the product portfolio and the sales team. Furthermore, every M&A involves ego, both on the part of the seller and the buyer. More often than not, what destroys the value of an acquisition is a misreading of the acquired company's culture.

However, Sinqia was able to show a lot of consistency in executing its acquisition processes. We keep in mind that one of the main reasons for this is identifying opportunities.

There are two ways to prospect new businesses, the first is through a boutique or investment bank, and the second is through the creation of an internal M&A team.

Sinqia could execute its business prospecting strategy for a long time, developing this know-how in-house.

Often, acquisitions targets were companies that Sinqia knew in-depth because they competed in a specific vertical or by reference from their customers. However, only recently, we started to see more prospecting by boutiques.

Since Sinqia maintains a close relationship with its clients, one of the most significant competitive differential the company has is the assertiveness that each transaction has.

Even so, historically, the acquisition processes are relatively time-consuming. The process can take more than six months to complete between the first conversation and closing. Within an environment with more competition, this can get in the way. In addition, greater competition on price may begin to appear.

From a quantitative point of view, the advantage of making acquisitions is quite immediate, so the deals usually seem pretty appealing.

First of all, is the acquisition of goodwill. Let's assume that Sinqia acquires a company with R$100mn in sales at a multiple of 2x EV/Sales and that it has R$20mn in equity.

Goodwill on the acquisition is the difference between the amount paid and the equity value of the acquired company. In this case, R$180 million (R$200mn - R$20mn). From an accounting point of view, the company can amortize this goodwill over ten years as an expense.

Although this expense referring to an amount already paid to the acquired company does not affect Sinqia's cash, it is subtracted from the income tax account. In other words, Sinqia earns a kind of “discount” by making acquisitions.

The image above is the representation of the example we commented before. In the acquisition process that Sinqia acquires a company for R$200mn, generating R$180mn of goodwill, there is a tax benefit with a present value of R$37.6 million.

The second quantitative advantage is cost savings. For example, when Sinqia makes an acquisition, there are cost savings with administrative, financial, and personnel management departments.

The final advantage is in the way you pay for an acquisition. Historically, Sinqia carried out acquisitions by paying in cash. However, over time, she began to pay a portion in cash and the remainder conditioned to the delivery of results within a period between three and five years.

With this, Sinqia improves its retention of the founders of the acquired companies, aligning the financial interest with that of the company.

In addition, the award also implies growth above what the company grew before it was acquired, bringing greater confidence to the business since the founder agreed to condition part of his receipt to this growth.

Risks

We understand that Sinqia's greatest risk is related to assertiveness in acquisitions (quality and price), in the ability to have time to market (be ahead in innovation), and in the way of allocating capital (organic, inorganic, dividend, or buyback).

After evaluating most of Sinqia's acquisitions, we understand that those made to acquire market share are valued at the fair price of the asset and that the financial gain comes through cost savings (synergies) and goodwill amortization.

We understand that there is a risk of capital allocation by acquiring this company profile. Although the probability of success is high, the internal rate of return on these acquisitions has fallen over time.

Sinqia has gained a lot of financial muscle over the years. Consequently, the value per share with this type of investment decreases over time, even though it consumes significant management time.

On the other hand, M&A carried out for the acquisition of competence are less recurrent and need greater alignment with the seller (negotiating earn-out) to improve success. Still, their potential in cross-selling and up-selling is incredible.

In addition, these acquisitions improve Sinqia's ability to have a longer time to market in product launches. For example, we believe that Sinqia has all the necessary skills to anticipate demand from financial institutions, but it requires focus.

The impression is that there was a lot of pressure for capital allocation after the company raised almost R$1 billion after two equity offerings and one debt offering, which brings us to the risk of capital allocation.

We don't mind offering shares for acquisitions, but it is important that every offering is well dimensioned. We believe, in particular, that the 2019 offer was not. The same could be said of the last follow-on made in 2021, but Sinqia has already allocated virtually all of its cash.

For the shareholder, the result that matters is the free cash flow per share. When a company makes a share offering, it dilutes its current shareholder base and, consequently, the return per share is diluted.

A successful share offering is one in which, even considering shareholder dilution, the return per share is higher. However, in the case of Sinqia, we understand that the offer was inaccurately dimensioned due to the time the company took to allocate capital.

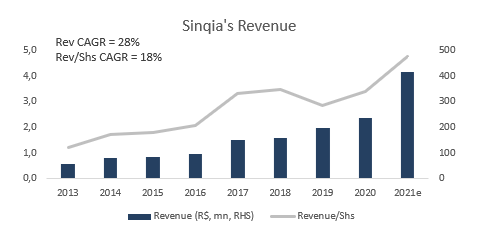

In the image below, we have a graph of the company's historical revenue and revenue divided by the number of shares outstanding. While the annual revenue growth rate was 28%, the growth plummets to 18% when considering earnings per share.

The average growth of 18% year-on-year is far from mediocre, but it took Sinqia two years to recover the same value it had in 2018.

Recently, Sinqia announced a plan to buyback 10% of its shares. It looks like an excellent capital allocation, given that the asset's rate of return is quite attractive.

However, according to the company's bylaws, it would be necessary to cancel the shares held in treasury to carry out new purchases. The impression is that the company is carrying the shares in the treasury, waiting for them to appreciate.

Looking at the company's equity rates of return, we believe that the best capital allocation would be to cancel these shares and continue the buyback plan, which would maximize the company's return per share.

Finally, if the company chooses to carry a relevant amount in cash, it might be interesting to reassess the debenture repurchase. With the Selic exceeding the 10% barrier, the cost of debt will soon exceed 15% (pre-tax).

Valuation

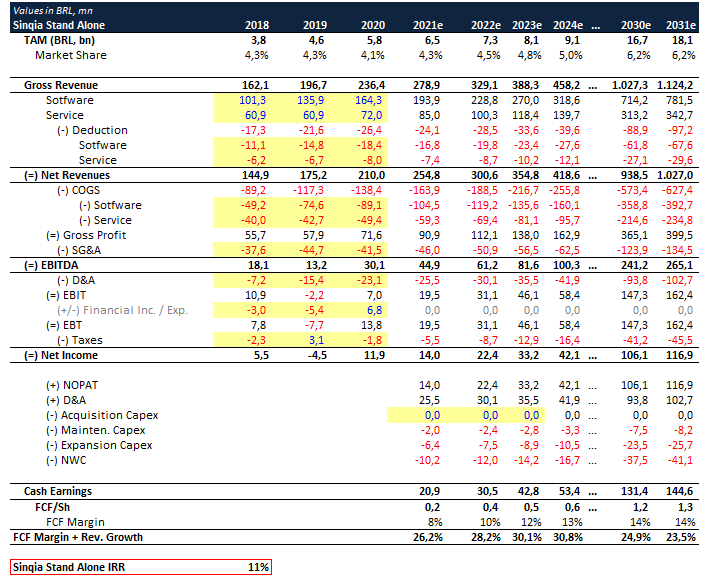

From the company's valuation point of view, the discount that Sinqia negotiates to its fair value is quite significant, even without considering any acquisitions made during 2021, as we will explain below.

In the image above, we assess the company considering only the results for the year 2020, excluding the acquisitions of Simply, FEP Web, Lote 45, NewCon, and QuiteJá.

We purposely penalized the company for acquisitions already carried out, removing more than R$100mn in revenue from the 2021 result and R$300mn from 2022.

The objective was to evaluate Sinqia's core operation, considering only the tipping of customers running legacy systems to the cloud.

Adding all the acquisitions and projections for each of them, we would have estimated revenue for 2022 of R$650mn and an Ebitda of R$180mn pro format, resulting in a much higher value per share.

Within an excessively conservative estimate, we see Sinqia trading something close to 10x EV/Ebitda 22e, with an IRR of 25%, delivering results consistently, good profitability, and capable of expanding its addressable market.

Also, it’s worth mentioning the Monte Carlo model we ran for Sinqia, showing that the company is wildly undervalued, even under extreme circumstances.

Password to Interactive Model: SQIA2022#

Disclosure: All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing/gambling your money.