Vale ($VALE)

Disclosure: All posts on Giro’s Newsletter are for informational purposes only. This post is NOT a recommendation to buy or sell securities discussed. So please, do your work before investing/gambling your money.

Access to Interactive Model.

Updated password is always available at Food for Thought

Today’s Outline

Tearsheet

Iron Ore Overview

Brief History

Revenue Sources

Ferrous Minerals

Base Metals (Nickel, Copper, and so on)

Competitive Position

Pricing Power

Capital Allocation

Valuation

Cash Earnings

Internal Rate of Return

Monte Carlo

Tearsheet

After a decade of divestments from non-core assets, and shrinking operations, mining companies have emerged since 2015, when commodity prices hit bottom.

Different from the past, the top players ( VALE 0.00%↑, Rio Tinto, BHP 0.00%↑ , and Fortescue) learned a valuable lesson about prioritizing capital allocation and choosing value over volume.

Oversupply is a loss-loss game while focusing on value (income) is a win-win for everyone.

Though Capex for mining companies could take several years to yield a positive return, the depletion curve for mines is relatively low so that the oversupply can perdure for years.

One interpretation is that mining companies have less volatile operational margins over time to focus on long-term projects.

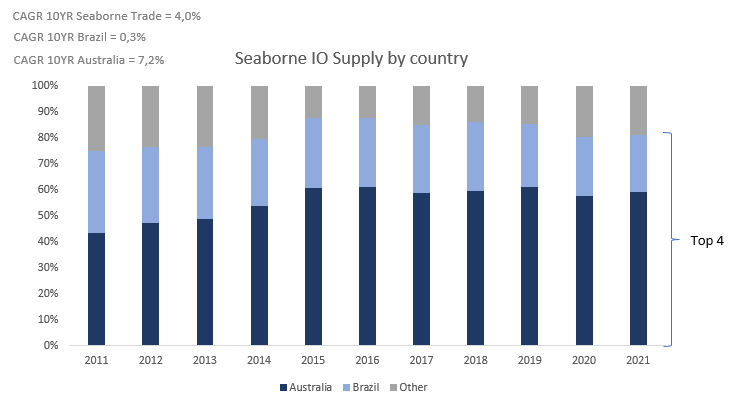

The win-win situation is possible only because the Seaborne market is concentrated, with the top four players being responsible for 70-80% of all seaborne supply.

Also, the cost curve for exploring iron ore is relatively steeper, different from the oil industry. Also, the increasing energy costs in the past years have been helping to widen barriers to entry.

The ESG agenda helps the industry's balance. China's environmental policies & reform of heavy industry limits China's domestic production.

Consequently, although the sector’s invested capital has declined for a decade (shrank 30% in the past ten years), the return on invested capital is almost hitting its all-time high.

Particularly for Vale, disruptions in Brazil, including long-term review of wet processing/ tailings storage, have been helping the company to focus on higher-margin products, especially after years of poor capital allocation.

However, it’s essential to have in mind a few risks, such as higher iron ore prices potentially incentive reactivation from marginal producers.

Unlike oil companies, mining companies have limited depletion/decline rates, so when incremental capacity can hit the market for years.

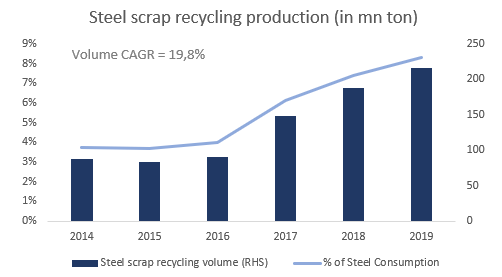

Also, steel scrap recycling production in China has been accelerating, growing above 20% CAGR in the past three years (excl. import).

All in, After a decade of divestments from non-core assets and shrinking operations, mining companies have emerged with a strategy of prioritizing profitability, not growth.

With over 70% of the seaborne market share in their hands, the top players might enjoy attractive returns on equity over the following years.

Nevertheless, it's essential to keep in mind that defragmented new players might pose a risk to supply stability and that alternative sources to iron ore might hit demand.

Iron Ore Overview

The global seaborne iron ore consumption comes from the northern hemisphere and supplies from the southern hemisphere.

Most iron ore (more than 70 percent) trades in the seaborne market, with relatively small volumes consumed domestically.

China is the largest iron ore importer, representing more than two-thirds of the total world trade in iron ore. We can split the legs-up in production in three: first between the 60s and 80s with Japan’s industrialization, second between 80s and 00s with S. Korea and Taiwan development, and finally, the last two decades led by China.

Asia represented around 90 percent of total seaborne imports in 2019 and 71% of all Iron Ore consumption to sustain its infrastructure and Real Estate industries.

Australia and Brazil are globally the leading exporters. However, Australia is the largest supplier, having shipped over 900Mn ton in 2021, exporting more than twice as much as that of Brazil, its primary competitor.

Australia has two advantages that are not replicable. The first is that Australian producers with a significant advantage in terms of proximity to the market, as freight can represent a sizeable proportion of the landed cost of iron ore.

In addition to the freight advantage, Australia enjoys the shortest lead time (14 days from Pilbara ports to Asia vs. 40 days sailing from Brazil to Asia), improving inventory management.

The second advantage is that Australia is supported with vast, high-quality hematite resources to produce low-cost, direct shipping ore (DSO) suited to modern mill requirements.

Iron ore resources can vary widely in grade. The most knows are i) Hematite (54-66% Fe), ii) Itabirite (30-45% Fe), and Magnetite (16-35% Fe). The highest grande Hematite ores come from Vale Brazil’s Northern System and BHP’s Mt Whaleback mine to less than 20 percent Fe for most of China’s low-grade magnetite.

Iron ores are rocks and minerals from which metallic iron can be extracted. There are four main types of iron ore deposit: massive hematite, which is the most commonly mined, magnetite, titanomagnetite, and pisolitic ironstone. These ores vary in color from dark grey, bright yellow, or deep purple to rusty red. Iron is responsible for the red color in many of our rocks and the deep red sands of the Australian deserts. (BHP IR Website)

Australian and Vale’s DSO operations typically have ore to product ratios around 1.2:1, compared to 5:1 typical in many Chinese magnetite mines. So superior products that enable the rapid expansion of minor ore require mining and processing for a tonne of the finished product.

Brief history

The Brazilian Federal Government ("Brazilian Government") decided to assemble Vale do Rio Doce (“VALE,” “Vale”) in 1942 to exploit, trade, transport, and export iron ore from Itabira mines.

The company's privatization process began in 1997, with the issuance of 388.6mn participative debentures, not convertible into shares ("Participative Debentures").

The Participative Debenture guaranteed to pre-privatization shareholders, including the Federal Government, the right to participate in the revenue of the mineral deposits of Vale and its subsidiaries, not valued for purposes of setting the minimum price of the Vale privatization auction.

Keep reading with a 7-day free trial

Subscribe to Giro's Newsletter to keep reading this post and get 7 days of free access to the full post archives.