Why Value Investing?

There are essentially two reasons. First of all, there’s a performance issue. One is the statistical regularity that we know as the value premium.

Value stocks, on average, yield higher returns than growth stocks. And you want a strategy where you want the wind in your back. So that’s one of the reasons to become a value investor.

The second reason, of course, is the performance of some extraordinary investors—people like Walter Schloss, Jim Rogers, Seth Klarman, or Warren Buffet.

You want to be in the winning team, which looks like a very good team to be in. But there’s a second, more subtle reason to become a value investor.

And it’s that you’re going to utilize your strength, lever the knowledge you have in a particular industry, lever your expertise, and try to discover value in those areas where you know the most.

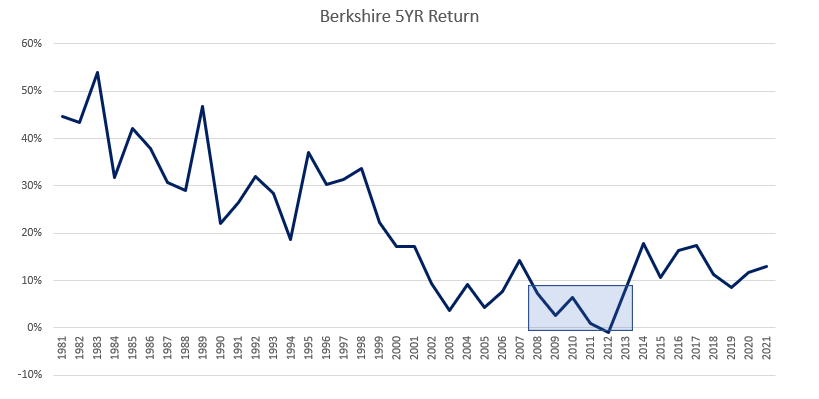

Consider, for instance, the performance of Warren Buffett throughout his famous career. You have the annualized returns you would have made had you invested with Mr. Buffett in any of those years.

Notice the extraordinary annualized returns you would have made had you invested with Warren Buffett in the early 80s.

Keep reading with a 7-day free trial

Subscribe to Giro's Newsletter to keep reading this post and get 7 days of free access to the full post archives.